The following are examples of folks that are likely to be found responsible parties through case law: a chief accountant and a controller that had unfettered access to the company's checking account. They, with knowledge of the payroll tax deficiencies, continued to write checks to other creditors and were found to be responsible parties. The treasurer of a corporation who knew that the corporate officer responsible for paying payroll taxes wasn't doing it was also found to be a responsible party. An officer of a corporation who delegated his duties to a general manager was also found to be a responsible party. An individual within a company who had final authority as to which checks got paid but delegated the actual cutting and signing of checks to subordinates was also found to be a responsible party. The business owner's spouse, who was the company's bookkeeper and had responsibility for writing all checks, was found to be a responsible party. On the other hand, the following are examples from case law where someone was not found to be a responsible party: a company secretary and assistant treasurer, who, however, was not a corporate officer, was not responsible for payroll taxes and had no knowledge they weren't being paid. The vice president of a company, who did not have authority to determine which creditors got paid and when, was not found to be a responsible party. The business owner's son, who didn't have independent authority to do anything in the business because of the type controls of his father but had the title of secretary and treasurer, was not found to be a responsible party. One of a company's largest shareholders, who had the apparent authority to decide who got paid but actually didn't participate in those decisions, was not found to...

Award-winning PDF software

Trust Fund Recovery penalty tax court Form: What You Should Know

Audit Services, Internal Revenue Service, P.O. Box 696, Joplin, MO 65802. (All fees are non-refundable.) Tax Adviser's Note: The tax adviser suggests that trust fund recovery penalty cases be processed by the agency's Compliance and Appeals Division. This has the benefit of avoiding the long, drawn out appeals process that can follow a case that has not been assigned to a case manager. The case manager may also have the advantage of being familiar with the case and its evidence. In order to avoid an adverse decision or adverse recommendation by a taxpayer's attorney, you would want to work with a compliance or appeals attorney before going to a court for the initial CDP. IRS Form 9150—Responsibility V:\PDF Forms\Documents\Responsibility Application. PD The above form must be returned through the mailed form (V:\PDF Forms\Documents\Responsibility Application). Tax Adviser's Note: The lawyer must also note in his client agreement that the trust fund recovery penalty is a civil penalty. For instance, see Rev. Pro. 1995-62, 1996-1 C.B. 489. This is not intended to restrict what can be filed in court as a penalty. A taxpayer who is liable for the trust fund recovery penalty by being found liable at the CDP should file IRS Form 3903, Application for Waiver of Fee. PD. Also, check with the taxpayer and/or the attorney to see what other options there are in pursuing the taxpayer's penalties. This includes taking the tax issue to an administrative law judge or a tax tribunal. Tax Advisory Bulletin 2009–16, Revenue Ruling 2009-8, Trust Funds: Trust Fund Recovery Penalty Cases in Appeals, provides additional information about the trust fund recovery penalty and other issues involved in the case. Also see Rev. Pro. 2002-12, 2003-1 C.B. 472. Trust Fund Recovery Notice — An IRS notice of a recovery of a taxpayer's unpaid tax liability that is based on a claim for a refund of the tax is a notice of an outstanding liability that is subject to seizure. The IRS sends a notice when it determines that a tax is due and that the taxpayer is liable to pay that tax. Note: If you do not owe tax, you do not have to take action (a notice of the liability).

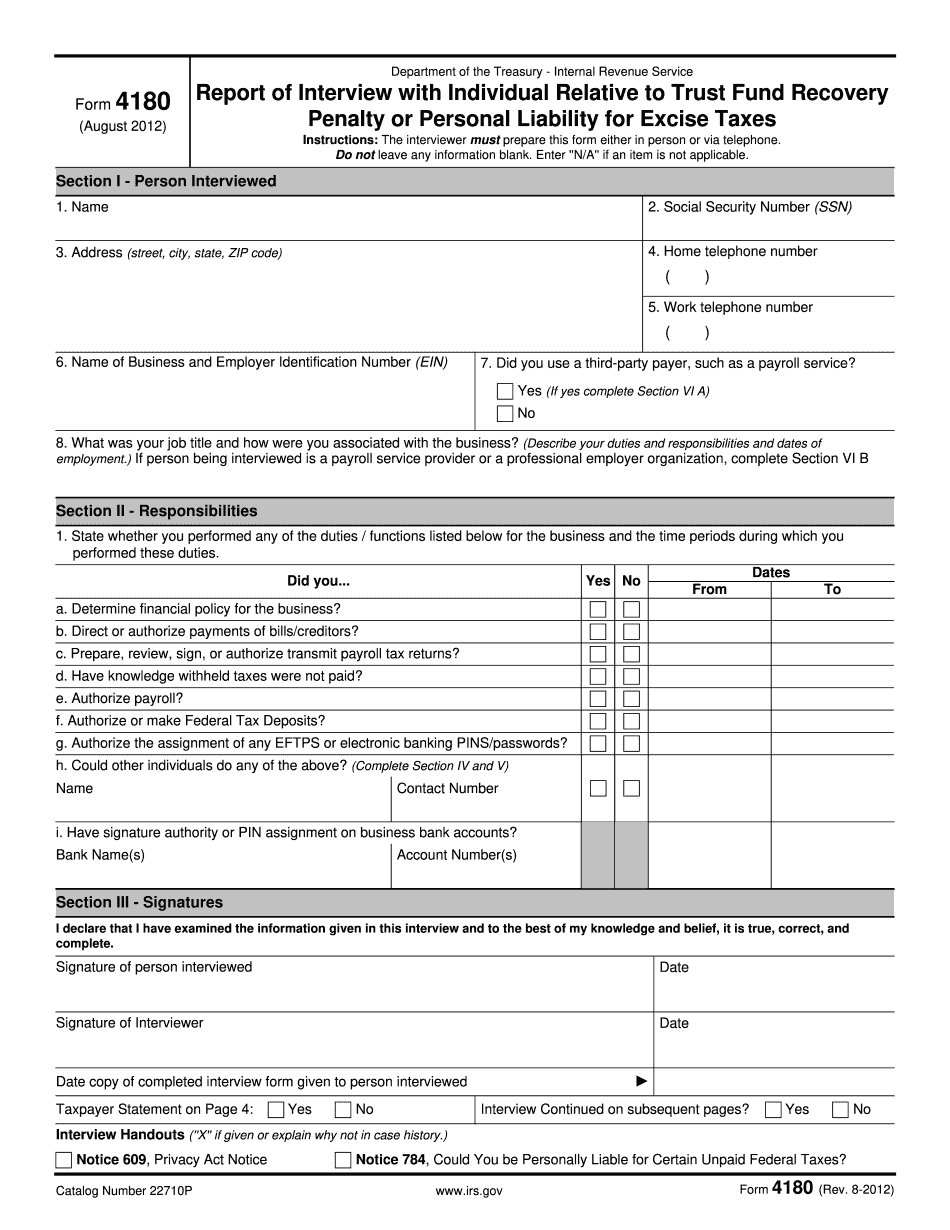

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 4180, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 4180 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 4180 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 4180 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Trust Fund Recovery penalty tax court