Award-winning PDF software

2848 trust Fund Recovery penalty Form: What You Should Know

O If the taxpayer was a participant in a qualified retirement plan, the penalty for non-sufficient funds is assessed on the date of the last day the taxpayer received a statement of employment (or the date specified under § 401(a)(17) that had been issued in connection with an individual retirement plan when the taxpayer last had access to the plan) showing the accrued benefit or allowance, less the amount of any excess contributions and penalty. The taxpayer must file an annual Form 5498(B) with the IRS by the due date of the Form 5498(B) or pay the penalty. O If the taxpayer received an individual retirement plan statement from the plan (or, as for a plan from a corporation, from its employer) reporting contributions, benefits, or pension or retirement account earnings when they were not accrued, then the penalty is assessed at the time of filing. The failure to timely file a report was the reason for the penalty, not the cause of the failure to maintain the plan in good standing. O If the taxpayer has a plan account with a custodian, the taxpayer must file a copy of the plan account statement with the IRS at least 14 days prior to the first day on which the IRS will assess the penalty. If the taxpayer is required to file a Form 5498 Notice with the IRS on IRS Transcript Cheat Sheet, the taxpayer must file a copy of the plan account statement with the appropriate IRS office. All failure to file forms (and/or failing to make timely annual Reports of Contributions, benefits, or interest) will result in the levy and a notice will be mailed to the taxpayer. The notice will also state that the penalty will be imposed. Directions for Refund of Trust Fund Penalty If the tax liability is paid without penalty, the IRS may pay it within 90 days of the date the payment is made, provided that the taxpayer files a timely return that includes all pertinent information. If the penalty has been paid within 90 days of the date the payment is made, the IRS is generally not required to pay the penalty, unless the taxpayer fails to file a timely return. If the taxpayer files a timely return and the return includes correct information on the liability, the IRS may refund the penalty.

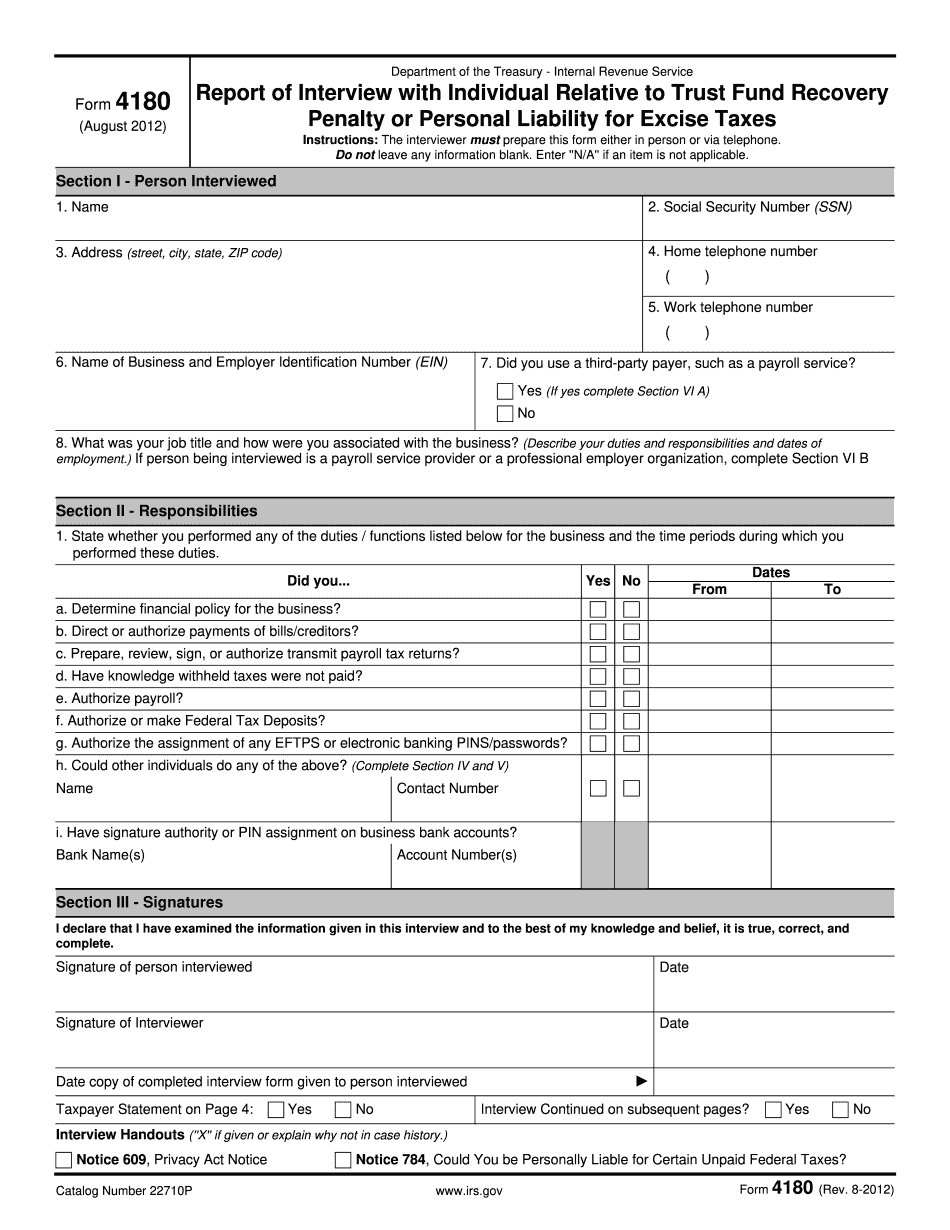

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 4180, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 4180 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 4180 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 4180 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.