Award-winning PDF software

Trust Fund Recovery penalty court cases Form: What You Should Know

Charge, as the taxpayer, was entitled to assert that the statute of limitations on her claim for relief (trust funds) was tolled while the Government waited to seek the funds, resulting in the tax and penalty. This appeal challenges the district court's decision to grant summary judgment on Mr. Edwards' charge, and to declare his trust-fund recovery Pledges to be fully paid and discharged. The Defendant Is Now Covered by the statute of limitations Cheryl L. Showman (U.S.) is a trust officer and agent. Ms. Showman is the administrator of two retirement Commissions (one pension and one deferred annuity). On November 20, 2008, the court granted a motion for summary judgment, and dismissed Ms. Showman's claim for the return of her trust funds. On April 11, 2010, the district court granted summary judgment against Ms. Showman on Mr. Porter's claims for the return of the trust funds. Ms. Showman appealed this decision to the United States Court of Appeals for the Eleventh Circuit. Background Information on the Trust Fund Recovery Penalty Program This program consists of a number of federal statutes and regulations that are administered by a U.S. Treasury Department which operates under the authority of Section 4985 of the Internal Revenue Code (IRC), as amended. IRS, under its authority and direction, can enforce these laws through the Civil Proceeding procedures of the Department of Justice. The following is generally not considered “tax fraud,” and does not qualify for recovery under the CPA, if it occurs prior to June 18, 2025 : • The taxpayer's act or omission did not affect the amount of the taxpayer's (or a related person's) liability and did not result in any tax. • The taxpayer's action or omission was not made willfully, maliciously, or in bad faith. This includes fraudulent attempts to claim the benefits, including taxes, granted to the taxpayer by the IRS and/or by the individual or family for which the taxpayer was liable.

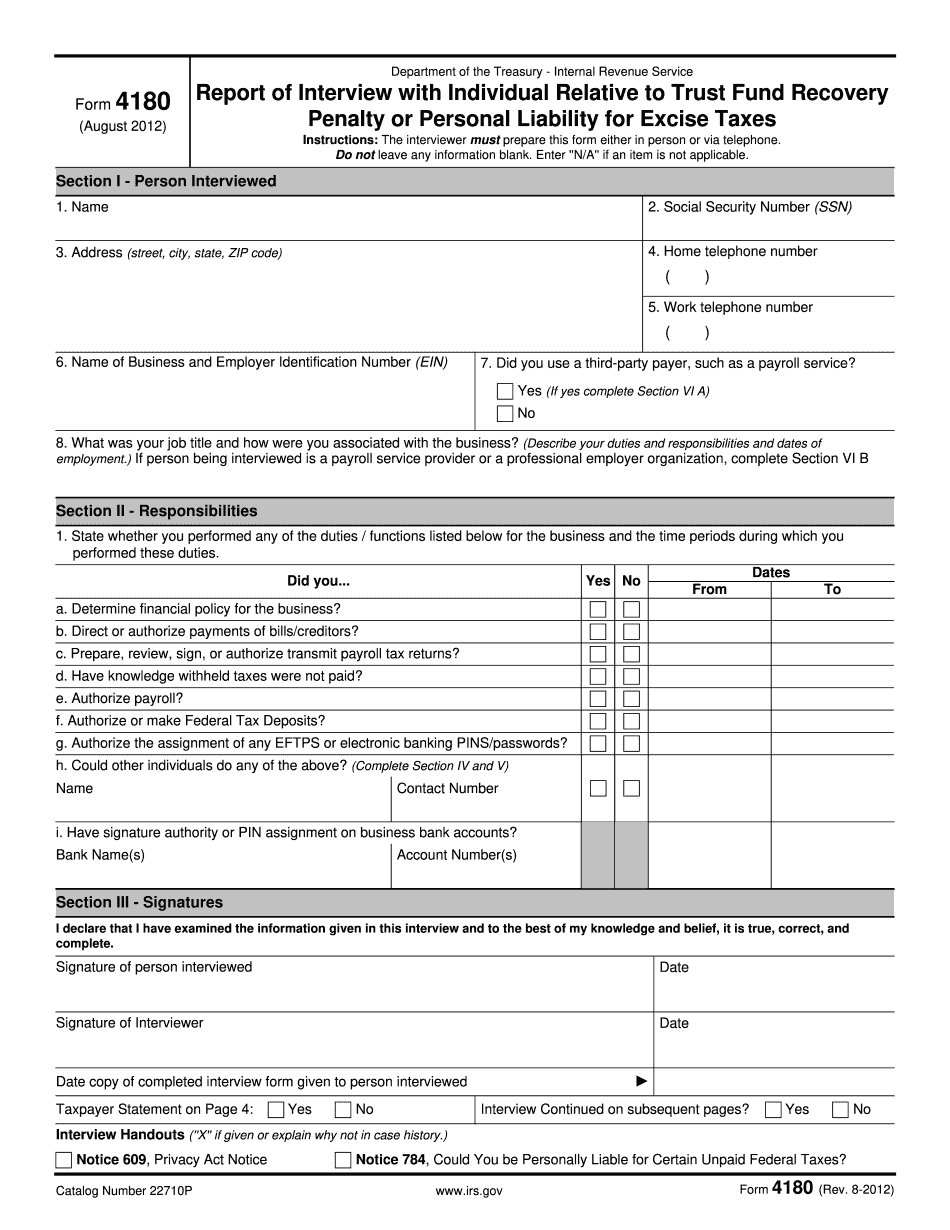

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 4180, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 4180 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 4180 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 4180 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.