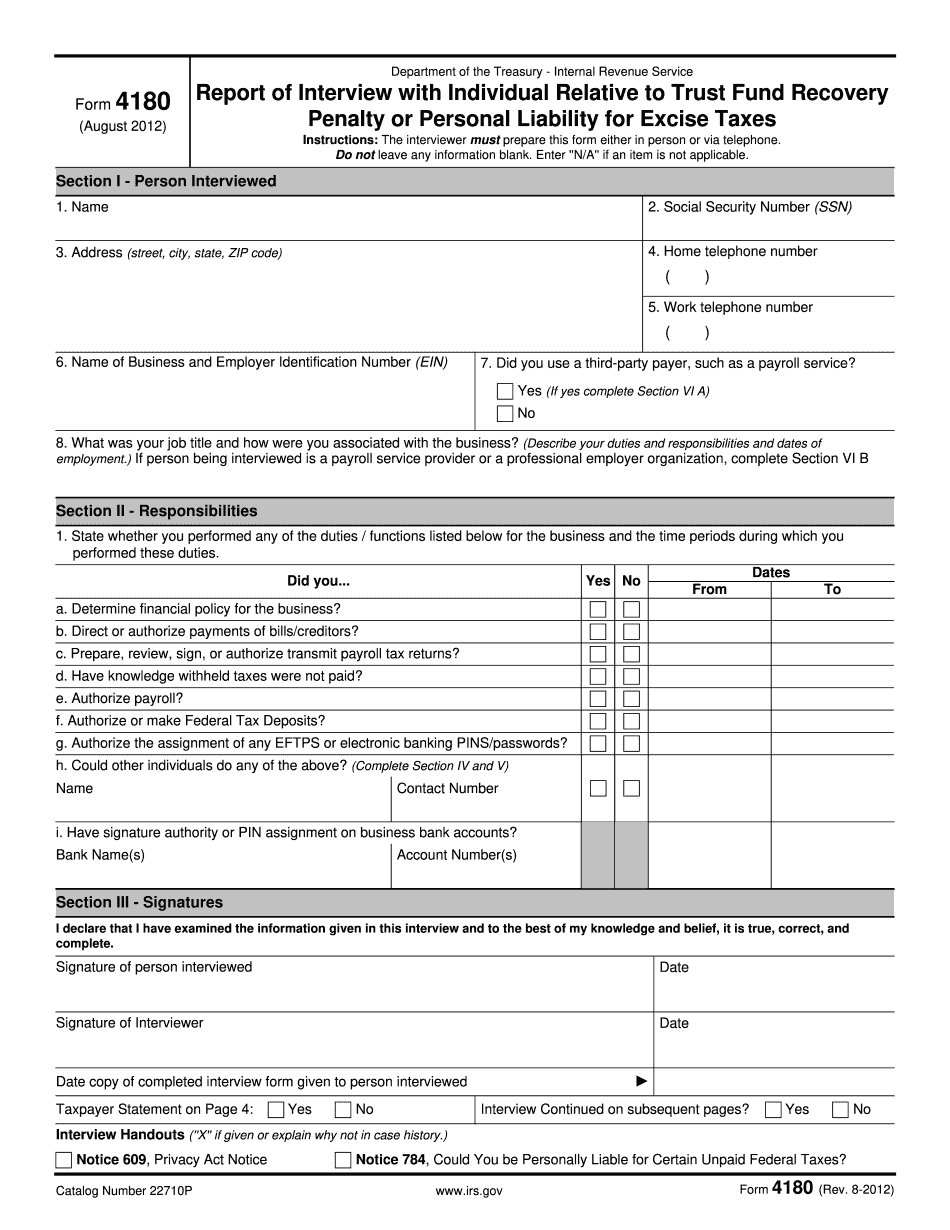

Let's discuss the process that a revenue officer goes through in making a responsible party determination. The first thing they're going to do is break out a form 4180, and they'll probably complete that with you sitting there. They'll be asking you questions and filling out the form. What they'll be doing is conducting an investigation to determine whether you have the responsibility to collect and remit payroll taxes. What's most important for you to realize here is if I am able to help you, or someone like me is able to help you, it's best to have representation during this responsible party interview. What I've been able to do successfully in the past is bring with me a body of case law where folks have been found responsible parties and not responsible parties. It's my job, if at all possible, to equate your case with all the cases where the party was not found to be a responsible party. That's the best way to deal with this if you're facing responsible party determination. I don't care if you have to pay for it yourself, you'll be a heck of a lot better off than being responsible for your employer's payroll taxes. What you need to know is that our OS determination is all it takes to be on the hook for that responsible party determination. You can appeal it, you can fight it, but all it takes to be on the hook for it, without having to find your way out of it, is that are owed to believe it. The statute of limitations for assessing a responsible party penalty is as follows: three years from the later of April fifteenth in the year of the final payroll taxes, or three years from the date the employment taxes were filed if later. When...

Award-winning PDF software

Trust Fund Recovery penalty statute of limitations Form: What You Should Know

Therefore, if you file a timely return with the IRS by Trust Fund Recovery Penalty — IRS The statute of limitations may be tolled by certain circumstances. For example, certain tax credits or deductions may be offset by periods of limitations. In addition, an assessment on the Trust Fund Recovery Penalty for an extension of the applicable statute of limitations is barred by a Trust Fund Recovery Penalty — IRS If you agree to pay the TARP tax on your own, you need not file a taxable income tax return. However, if you do not do so, the IRS may assess a tax on the amount it finds to be due. Taxes on Employee Benefit Plans (EBP) If you are The IRS can assess a penalty on any portion of the plan's plan taxable income, regardless of the amount of net earnings derived thereby. See Publication 519, Income Tax Withholding and Estimated Tax for more information. The IRS does not levy a penalty on distributions from an EBP to a participant's own account due to a payment for EBP (i.e., an employee loan) unless the EBP's tax treatment would impose a 500 annual tax penalty on the participant. However, see Publication 529, Payments to Qualified Plans for more information on the EBP. If you are a plan sponsor or an administrator of an EBP, an assessment on part or all of the plan's plan taxable income may also be imposed if the plan was established by a disqualified person. For more information on EBP, go to IRS.gov/EmployeeBenefits. Who Can Pay the Tax? Generally, individuals, partnerships, and S corporations must pay the TARP. If you have an entity (i.e., trust) whose earnings exceed a particular threshold, the entity may be liable for the tax in addition to any income subject to tax on the earnings. The IRS will not charge this penalty if a TARP payment exceeds the amount of the participant's compensation. Also, a TARP payment may not exceed the amount of any contribution or other deduction made to the plan. The IRS doesn't charge this penalty if you make the payment with respect to an individual who is not subject to tax. For example, if you make a TARP payment of 2,000 for health coverage, this amount is not subject to tax.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 4180, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 4180 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 4180 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 4180 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Trust Fund Recovery penalty statute of limitations