My name is Patrick Sheehan, and I am a former IRS attorney. What happens when the IRS comes after you related to your business taxes? When a corporation has unpaid employment tax liability to the IRS, and if that corporation can't pay the money fast enough, the IRS might assert something called the trust fund recovery penalty against the owners, the officers, the shareholders, the people who really run the business. By doing this, they expand the number of people that they can collect from. Until they do this, they can only collect from the business. But when they expand it under the trust fund recovery penalty, they can get the vice president, the president, the bookkeeper, the Board of Directors, the people who run the business. When the IRS proposes to assess the trust fund recovery penalty against you, they send a letter, and the letter gives you 60 days to file a protest. Again, deadlines are very, very important. You can't miss any deadlines because if you don't file a timely protest, then the IRS is gonna say we were right, and then they're gonna send a bill and then start collecting money from you, even if you weren't really meaningfully involved in that business. How do you defend against the trust fund recovery penalty? There are two arguments that we make. One is responsibility or willfulness. Responsibility means that you actually made the decisions that led to this unpaid tax liability. You preferred to pay a creditor to keep the doors open instead of paying the money to the IRS. A lot of people have someone who runs the business back in the office and someone who's out making the calls. So the person out making the calls doesn't necessarily know what's going on back at the office....

Award-winning PDF software

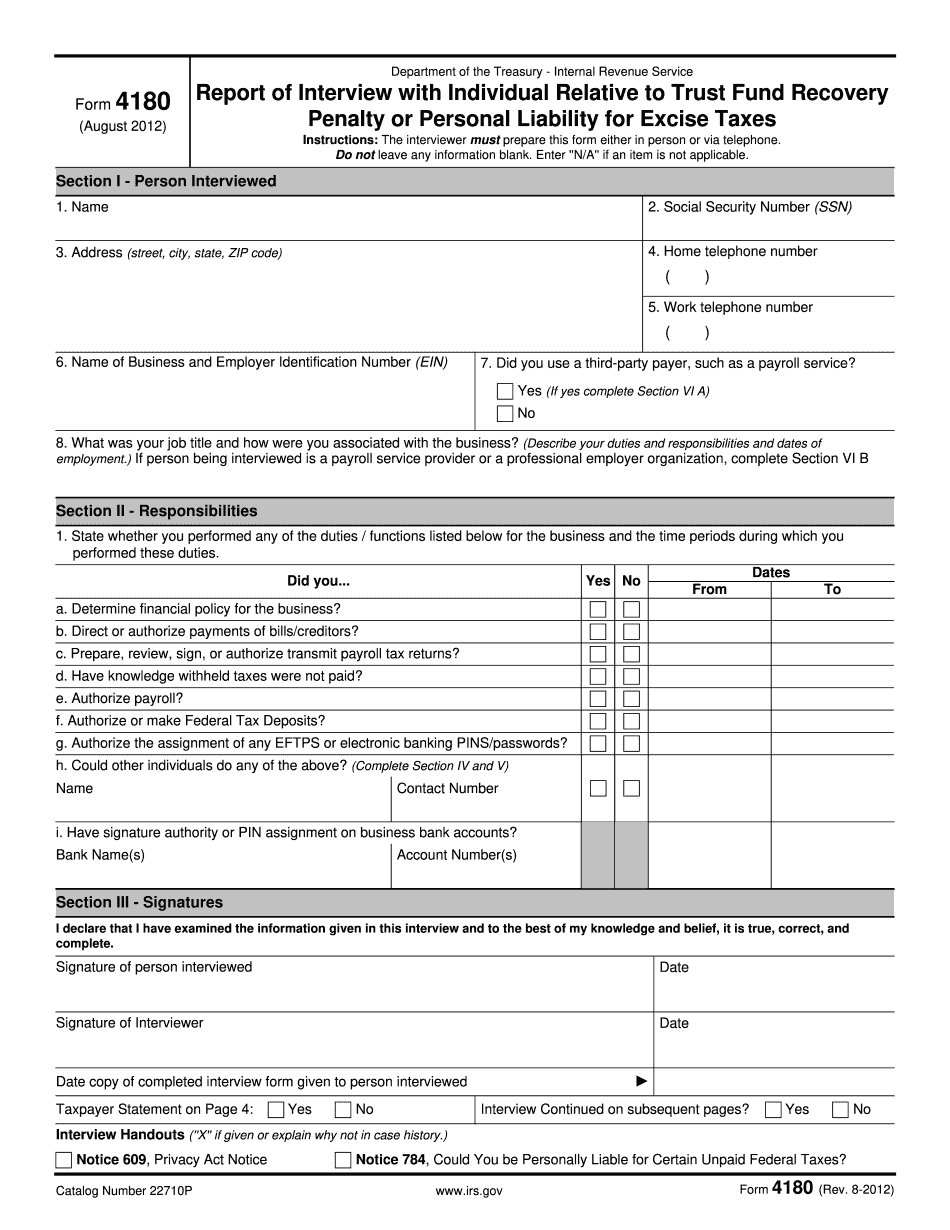

How to avoid 4180 Interview Form: What You Should Know

Investigation and Recommendation — Taxpayer If you have not received an IRS letter, and are still the target of a 4180 investigation, take the following steps : If you are in the IRS field and still in tax school, make sure you know enough to respond to the summons, request for a hearing, and file a Taxpayer Claim (Form 8919) in time for the investigation. You would need to have completed the course, if you had been in school for an extended period, so you can handle the form properly. The client will need to understand and be on the same page when it comes to all the following things that will go into the interview: 1) What the IRS has learned about you. 2) What the attorney and his client think. 3) What the agency has found. To whom, to what, and why. 4) How the attorney and his client feel about these findings. 5) Do you feel confident you are innocent of the Taxpayer Fraud? 6) The time frame for submitting the 4180. 7) How can the client obtain a “reasonable attorney” when the Taxpayer Fraud and Fraud Taxpayer Protection Act was enacted. 8) If the attorney and his client, like themselves, believe you will be targeted for prosecution, and what happens if they are targeted themselves. 9) What can the attorney and his client do to protect themselves and their client from any criminal prosecution. 10) What is a “reasonable attorney” and what can he do to obtain one for his clients? A “reasonable attorney” could consist of anyone that knows the facts of the case better than the IRS. 13.5.5 What to do if you have been identified as the tax return preparer in a case where they are targeting you. We have included several resources (links) if you need clarification on this or any other questions. 13.5.6 Taxpayer Protection Act Questions for Non-Representation There are very few tax practitioners that are aware of what the Taxpayer Protection Act means, and what it might mean to them. For more information: U.S. Treasury: TPA and IRS Form 8919 (Form 4868) Internal Revenue Services Bulletin 654, Taxpayer Fraud and Taxpayer Protection Act: Information for Tax Professionals: The Taxpayer Protection Act.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 4180, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 4180 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 4180 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 4180 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing How to avoid 4180 Interview